Occupational pension provision: full insurance solutions versus semi-autonomous collective foundations

AXA will no longer offer full insurance from 1 January 2019. What are the consequences and what alternatives are there?

With its announcement of 10 April 2018, AXA Switzerland informed that it was withdrawing from the business with full insurance policies in occupational pensions and converting the existing full insurance foundations into partially autonomous foundations as of the beginning of 2019. In accordance with the decision of AXA Switzerland and the Boards of Trustees, the insurer will in future focus on semi-autonomous pension schemes in which the companies bear the investment risk themselves.

Following the withdrawal of AXA Switzerland, Allianz Suisse, Swiss Life, Helvetia, Baloise and Pax will continue to offer full insurance for occupational benefits. All five underline their intention to continue to offer the entire range.

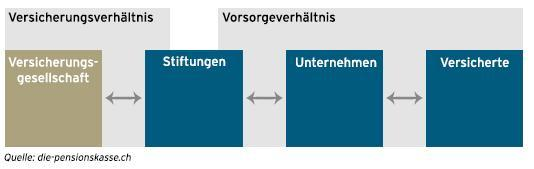

An overview of the organisational forms of occupational benefits

Full insurance

Features of comprehensive insurance

Full insurance policies are foundations of a life insurance company which are partially autonomous, but have reinsured all risks 1:1 with a life insurance company. In addition to the risks to be insured in accordance with the law on occupational benefits (BVG) - old age, death and disability - the insurance company also assumes the financial market risk. The insurance company is also entrusted with the administrative implementation.

The advantage here is a guaranteed pension benefit without the risk for employer and employee of having to bear additional restructuring costs in the event of underfunding. In order to be able to guarantee this security, the insurance companies in the LPP/BVG business are subject not only to LPP/BVG and BVV2 legislation but also to stricter supervision by FINMA. This is in contrast to collective institutions, which are only subject to BVG supervision.

Security comes at a price: since this model prohibits underfunding, the insurance company must invest the pension assets entrusted to it in an extremely conservative manner. This results in a limited return on investments - and thus on the pension capital. Losses are borne by the insurance company and thus by the shareholders.

For whom is a full insurance solution interesting?

Full insurance is particularly suitable for SMEs that are unable or unwilling to manage their own autonomous pension fund. These are often employers who can only afford the BVG solution without supplementary insurance in the non-mandatory area. Priority is given to the desire not to have to bear any investment risks and to be able to implement the BVG simply.

Model of full insurance

Semi-autonomous collective foundation

Features of a semi-autonomous collective foundation

Consists of economically and organizationally separate pension funds from different employers, each with its own regulations.

In the case of semi-autonomous collective foundations, the savings portion is often managed independently and individual risks are transferred, i.e. the risks of death and disability are reinsured. Reinsurance is provided by a number of large insurance companies and companies specialising in reinsurance. Affiliated companies and their insured persons bear any gaps in coverage on the investment side, although temporary undercoverage is also permitted.

Overview of some advantages of semi-autonomous collective foundations

Lower risk premiums: Policyholders benefit from risk premiums that are approximately 1/3 lower.

Higher interest: Because of the strict investment corset, full insurance policies invest two thirds of their capital in mostly low-yield bonds. Semi-autonomous collective foundations can invest much more in shares and less in bonds. In good stock market years, the income generated with the vested benefit credit thus increases more strongly.

Lower administrative costs: insured persons can expect lower administrative costs.

Community Foundation

Characteristics of a community foundation

The individual financial statements are not separated in accounting terms. They have common regulations and common pension assets.

Autonomous Foundation

Characteristics of an autonomous foundation

Carries all risks 100 %. The entirety of the fund members form the risk community - as a rule, these are the company's employees.

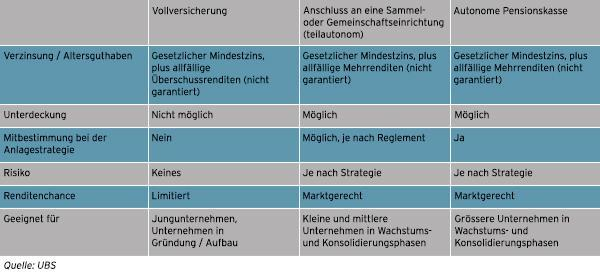

A direct comparison of pension solutions

Outlook

"Occupational pension schemes, together with the AHV / IV, should enable elderly, surviving dependants and disabled persons to continue their accustomed standard of living in an appropriate manner". A constitutional mandate whose implementation is becoming increasingly difficult with the prevailing legislation.

The bill on the reform of old-age provision (Federal Law on the Reform of Old-Age Provision 2020) was rejected in the referendum of 24.9.2017. The aim of the reform was to secure pensions and adapt old-age provision to social developments. Today it is a fact that an increasing share of the investment success must be used for the cross-subsidisation of old-age pensions. This is exacerbated by the 6.8 % conversion rate in the BVG mandatory, which is too high and takes no account of the returns achieved on the financial markets or of current age expectations. Politicians are called upon to come up with proposals for solutions in a timely manner.