In the summer, SUVA announces the premiums for the coming year – invest time in checking the details, it may be worth it!

No one likes to pay too high insurance premiums. Once a year, SUVA sends updated classification notices to companies that are subject to this institution. The premiums for the coming year are announced with these notices. We will show you how your company can review optimisation opportunities.

Why is my company insured with SUVA and not with a private insurer? What are the premiums for occupational and non-occupational accidents? Can I reduce the premiums? What can I do if I do not agree with the ruling? In the following article, we shed light on these topics and make suggestions on how you can achieve a possible premium reduction.

Every year - usually in the summer months of July/August - SUVA ("Schweizerische Unfallversicherungsanstalt", Swiss Accident Insurance Fund) issues the classification regulations that form the basis for occupational and non-occupational accident premiums for the coming year.

What do the companies have to do? In payroll processing, it is important to ensure that the premiums for the next year are recorded and applied in the payroll system so that the payroll deduction for the premium amount is correct. Is that all there is for the employer to do? No, because it is possible to check whether the conditions on which the premium calculations are based are still correct. Keeping premiums low is in the interest of every company because nobody likes to pay high premiums voluntarily. So are there ways to influence the rate of premiums? Yes, in the following paragraphs we will show you what you can do as a company. First, we will explain the reasons for being subject to SUVA and the general composition of the premiums.

Why is my company subject to SUVA and not to a private insurer?

According to Art. 58 ff UVG (DE, FR, IT), companies are insured either by SUVA or by other authorised private insurers. This system is called multiple insurer affiliation. Since the law and the ordinance specify exactly which establishments are covered by which insurer, there is basically no right to choose. We are now interested in knowing which companies are covered by which insurer.

Art. 66 Abs 1 UVG (DE, FR, IT) bindingly regulates which companies fall under the scope of SUVA. This leads to the remaining companies being assigned to private providers based on the exclusion principle.

How are the premiums determined?

Risk pools are formed for the purpose of setting premiums in relation to occupational accident insurance. In such collectives, the same types of business with the same activity and thus a similar accident risk are grouped together (e.g. scaffolding). Furthermore, the following are included in the calculations:

- the operational conditions, which are documented by means of a description of the company (DE, FR, IT)

- the annually supplemented risk reports, which include the number and costs of accidents in the company

- the classification rules (DE, FR, IT), i.e. the levels and rates of the premium tariff

What is the actual composition of the gross premium?

The premium is determined as a percentage of the payroll total. It consists of the net premium for the expenditure on insurance benefits and the surcharges for prevention and administrative costs. In addition, interest surpluses and surcharges for inflation allowances are taken into account depending on the capital yield situation.

Who has to pay the premiums?

Art. 91 Abs 1 UVG (DE, FR, IT) stipulates that premiums for occupational accidents and diseases are to be paid by the employer.

Art. 91 Abs 2 UVG (DE, FR, IT) stipulates that the premiums for non-occupational accidents may be charged in full to the employee. However, agreements in his or her favour are permissible.

What premium models are available?

Based on the size of the company, the following three different premium models (DE, FR, IT) are used, which are based on a uniform assessment system. The assignment to the respective model is determined by the premium volume of the company.

- basic rate for smaller businesses

- bonus-malus system for medium-sized businesses

- experience tariff system for large companies

Let's return to the initial question: What can the company do to keep accident insurance premiums as low as possible?

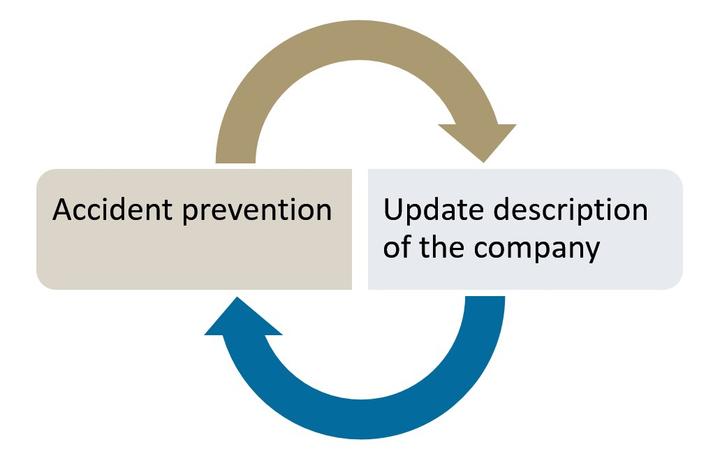

Prevent accidents

Targeted accident prevention keeps premiums stable:

Accident prevention (DE, FR, IT)

Update the operational description (activity, operational characteristics)

- Check the ratio of administrative to operational staff. It is not the number of employees that is decisive but the total wages.

- Has the type of work changed? Adjust the description.

If the parameters of the original information have changed, this can lead to a considerable premium reduction in the best case.

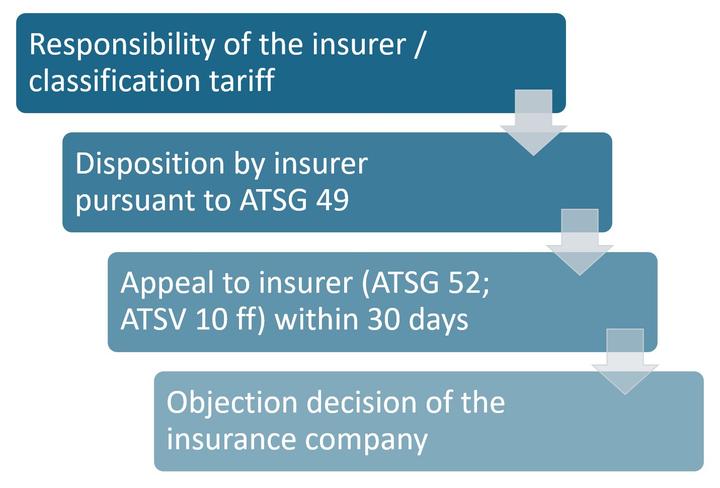

What do I do if I do not agree with the classification decision?

The legal regulations stipulate that an appeal against the classification order can be filed at SUVA within 30 days and must be justified and signed in writing. The process for the ruling and subsequent objections / appeals is described below:

Do you have questions about accident insurance and the accident insurance supplement? Do you have questions about the premium-relevant payroll total or are you looking for support in analysing the classification order and updating the company description? We are happy to support and advise you at any time on all social insurance matters.